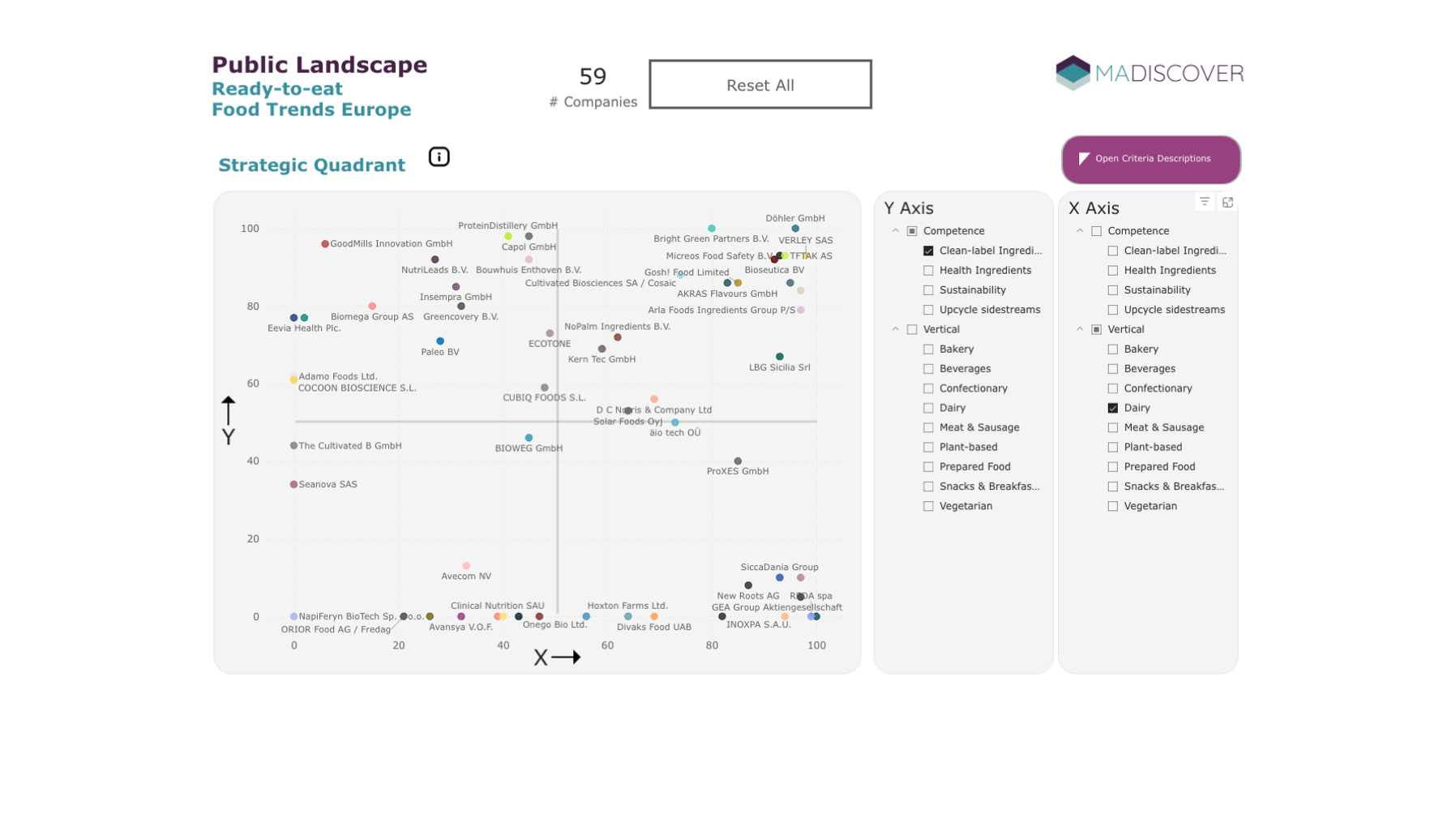

The industrial food processing industry below the consumer brands is hugely diverse and in motion.

Who are the companies behind the burger paddies, the milkshakes and the fries?

Who takes a bet on the growing plant-based niche?

What other food trends are on the rise in the ready-to-eat food value chain?

Some key learnings:

- Upstream in the value chain, particularly among machine builders, the market is dominated by older, well-established players. These companies have the personnel depth and financial strength required to succeed in an asset-heavy position.

- At the other extreme—end-product manufacturing—especially in trending food categories, the landscape is largely shaped by start-ups and younger companies. Entry barriers are lower in terms of initial investment, but competition is intense, with many players offering similar products.

- The positions in between also represent a “middle ground” in terms of company size and lifecycle stage. Ingredient manufacturers and process engineers are often niche players with already substantial revenues and focused market positions.

Martin’s high-level conclusion:

There’s no single “best” place in the food value chain—just different risk–reward profiles.

If you’re looking for high risk, high reward, end-product manufacturers are worth a closer look.

If you prefer lower risk and broader market access, earlier value-chain positions may be the better bet.

Do not hesitate to contact us to get a free guide through the depth of the MADiscover landscape: martin.beimler@madiscover.com

Search Scope

Value chain of ready-to-eat food food trends

Geography

Headquartered in the EU

Screening Criteria

Competence: Clean label ingredients, health ingredients, sustainability and upcycling side streams

Applications: Bakery, Beverages, Confectionary, Dairy, Meat & Sausage, Plant-based, prepared Food, Snacks & Breakfast, Vegetarian

Value Chain: Machine Builder, Process Engineer, Ingredient Manufacturer, Contract Manufacturer, End Product Manufacturer